Keep Your Eye On The VIX, It May Be A Useful Indicator For Stock Pickers

Summary

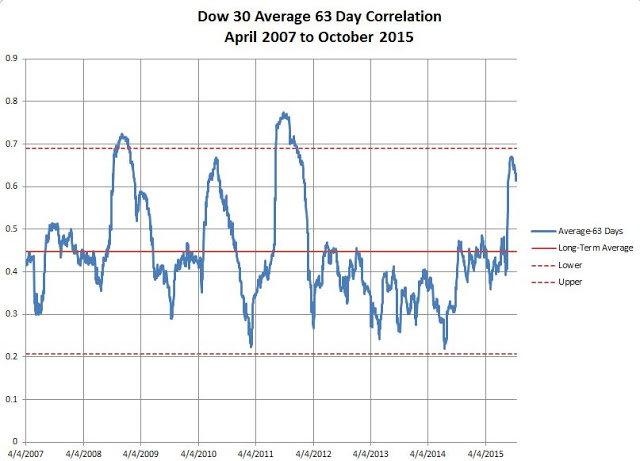

The average correlation of the Dow Jones 30 changes over time ranging from a low of 0.22 to a high of 0.78. This is the average of the pairwise correlations over 63 trading days..

Lower (higher) correlations may be associated with better (worse) stock picking performance.

Higher average correlations seem to be moderately associated with a higher VIX index.

The VIX may be useful in forecasting the average correlation.

An interesting quantitative technique for understanding equitiey market dynamics is to look at the average correlation of a group of stocks or of an index. My hypothesis is that when the average correlations are high, stock pickers have a harder time beating a broad market index. When average correlations are low, stock pickers have more of an opportunity to beat the market. By average correlation I mean the average of all the pairwise correlations of equities in a benchmark.

I decided to use at the Dow Jones Industrial Average which contains 30 stocks. The companies are:

I downloaded daily prices from Yahoo Finance going back to April 2007, calculated daily returns, and used this database for my analysis.

I calculated the average correlation over 63 days , which is one quarter, as there are 21 trading days in a month. The chart is shown below. I also included the long-term average (the average of all the time periods) and the standard deviation. The long-term average is 0.45 and the standard deviation is 0.13. I added lines for two standard deviations above and below the mean.

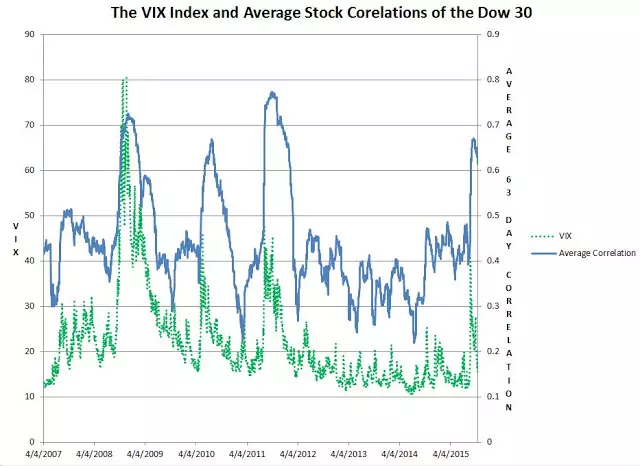

The chart shows significant periods when the correlations were high; recently the correlations have been in the .6 to .7 range, well above the long-term average. From April 2012 to October 2014 the correlation were consistently low. I thought that the chart pattern might be correlated to volatility, so I have included it in the next chart. The green dotted line is the level of the VIX measured on the left axis. VIX is the ticker for the Volatility Index published by the Chicago Board Options Exchange and is sometimes referred to as the fear gauge. It is a measure of the implied volatility of the S&P 500 index and as such is one measure of market volatility.

A quick look at the chart seems to indicate that when the VIX is high, so is the average correlation. The VIX accounts for 49% of the variance in the average correlation series, which represents a correlation of 0.70.

I next conducted a causality test proposed by the late Nobel economist, Clive Granger. One variable is regressed against the other and then vice versa. If there is a causal relationship, then one can say that one variable “Granger causes” the second. All this means is that one variable is useful for forecasting another. Most times a Granger causality study is inconclusive as it typically shows that neither variable is useful in forecasting. The null hypothesis is that a variable is not useful in forecasting another. So when a probability value for the test is smaller then .05, it means that we can reject the null and accept that there may be a useful forecasting equation. When I ran the test the result was that knowledge of the VIX was a good predictor for the average correlation and that the relationship was one way from the VIX to the average correlation.

There are several areas for future research. First, use a broader index like the S&P 500 or the Russell 1000. Second, I need to find a database containing a time series of median manager returns. This would help in proving or disproving my hypothesis that stock pickers have better performance when the average correlation is low.